Energy Shock Reshapes the Global Economic Balance

The escalation of tensions with Iran is rapidly transforming energy markets and exposing structural vulnerabilities across major economies. While the immediate reaction has been a sharp surge in oil and gas prices, the broader economic consequences will not be evenly distributed. In fact, the global economic burden of this conflict is likely to fall disproportionately on Europe and Asia, while the United States may emerge relatively less exposed, thanks to its transformation into an energy superpower over the past decade.

The result is not merely an energy shock — but a global redistribution of economic pressure.

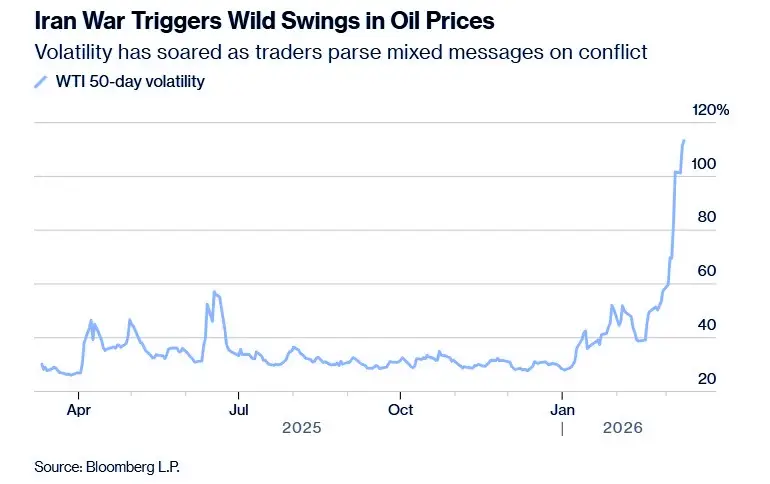

Energy Prices Surge as Hormuz Risk Returns

The outbreak of conflict has reignited fears surrounding the Strait of Hormuz, one of the most critical energy chokepoints in the world.

Markets quickly priced in the possibility of supply disruptions:

- Brent crude surged close to 30% in a single week

- European natural gas prices jumped by nearly two-thirds

- Oil briefly traded above $115 per barrel

Even if physical disruptions do not materialize immediately, the risk premium alone is sufficient to keep prices elevated.

And historically, energy shocks of this magnitude tend to trigger three immediate macroeconomic effects:

- Higher inflation

- Weaker household purchasing power

- Slower economic growth

For central banks that were preparing to ease monetary policy in 2026, the timing could hardly be worse.

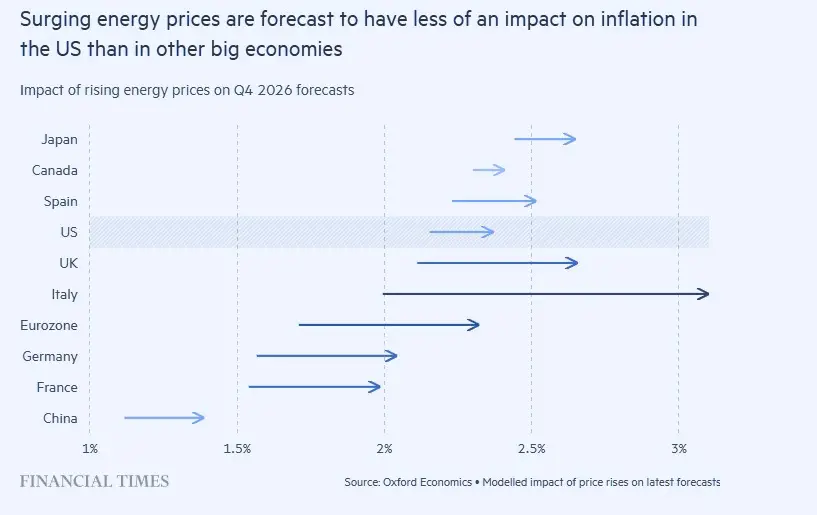

Europe: The Most Vulnerable Major Economy

Among advanced economies, Europe appears to be the most exposed to the current energy shock. Unlike the United States, the European economy remains heavily dependent on imported energy — particularly natural gas.

Countries such as:

- Germany

- Italy

- United Kingdom

are especially sensitive to gas price volatility because gas remains a central component of their power generation and industrial activity. Economic simulations suggest that Italian inflation alone could rise by more than 1 percentage point due to the energy spike, while inflation across the Eurozone and the UK could increase by more than 0.5 percentage points. This complicates the policy outlook for the European Central Bank

Asia: Energy Dependency Amplifies the Shock

The energy shock is equally significant across Asia. Large manufacturing economies such as:

- China

- India

- South Korea

remain heavily dependent on imported oil and gas — much of which flows through the Strait of Hormuz. China alone imports roughly 70–75% of its crude oil consumption, with a substantial portion sourced from the Middle East. However, China may be better positioned to manage the shock through:

- Large strategic oil reserves

- The ability to control domestic fuel prices

- Access to alternative supplies from Russia

Interestingly, slightly higher inflation may even help China counter the persistent deflationary pressures that have weighed on its economy over the past year.

The US: Insulated — But Not Immune

The United States occupies a unique position in this crisis. Thanks to the shale revolution, the US has become:

- The world’s largest oil producer

- A net exporter of natural gas since 2017

- A net exporter of crude oil since 2020

This structural shift offers a partial economic buffer. Higher energy prices can actually support US production, investment, and export revenues, offsetting part of the economic damage. However, American households will still feel the impact through rising fuel costs. Petrol prices have already climbed above $3.30 per gallon, and could move higher if oil prices remain elevated.

This presents a political challenge for the White House, especially as rising fuel costs disproportionately affect lower-income households — a sensitive issue ahead of upcoming elections.

Winners and Losers: Energy Exporters Benefit.

While energy-importing economies face inflationary pressure, some countries stand to benefit from the surge in prices. Major exporters such as:

- Norway

- Canada

could experience a clear economic upside as they capitalize on stronger energy revenues without facing the geopolitical risks confronting Middle Eastern producers.

In essence, the energy shock acts as a global income transfer — shifting wealth from energy consumers toward energy producers.

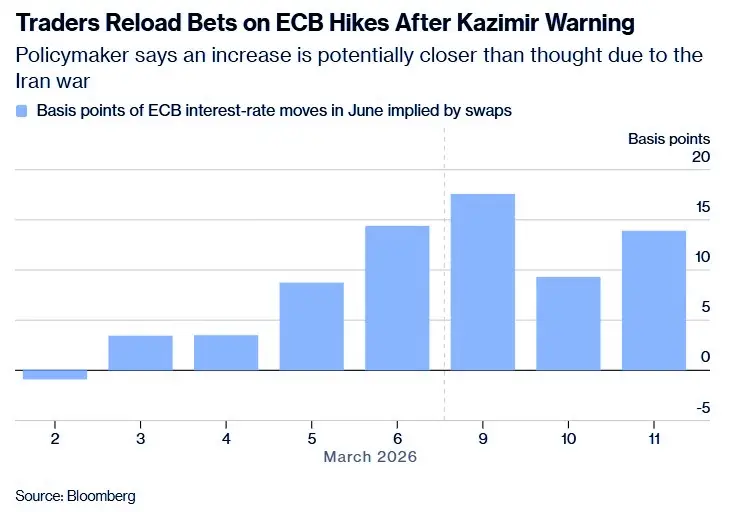

Central Banks: Rate Cuts Now in Question

The inflationary implications of higher energy prices are already reshaping monetary policy expectations. Markets are beginning to reassess the pace of policy easing:

- The Federal Reserve may delay rate cuts.

- The ECB could adopt a more cautious stance.

- The Bank of England may keep rates elevated longer than previously expected.

In other words, the energy shock could extend the global high-rate environment, adding another layer of pressure on growth.

Bottom Line: A Global Shock with Uneven Consequences

The Iran conflict is not simply a geopolitical event — it is a macro shock reverberating through energy markets, inflation dynamics, and monetary policy expectations.

While every economy will feel the impact, the distribution of pain will not be equal.

- Europe and Asia face the greatest inflation and growth risks due to energy dependence.

- The United States remains relatively insulated thanks to domestic energy production.

- Energy exporters could emerge as the unexpected beneficiaries.

The key variable now is DURATION.

If tensions escalate or shipping through the Strait of Hormuz becomes disrupted, the current energy spike could evolve into a much deeper global economic shock. That said, history suggests that prolonged conflicts become increasingly difficult to sustain when oil prices remain elevated — the same revenues that empower energy exporters also generate intense economic and political pressure on all parties to seek resolution. In that sense, high prices may themselves contain a built-in incentive for a shorter conflict.