From Iraq to Iran: A War Trump Promised Not to Fight

One of the central pillars of Donald Trump’s political rise was his rejection of America’s post-9/11 war doctrine. On the campaign trail, Trump repeatedly returned to one argument: the United States had spent trillions of dollars fighting wars—especially in Iraq—while neglecting its own economy.

He framed Iraq as the ultimate example of strategic waste. According to Trump, the money spent on that war could have rebuilt American infrastructure, revived manufacturing, and strengthened the middle class. War, in his narrative, was not only morally questionable, it was economically destructive.

This is what makes the Iran question so politically dangerous. A direct confrontation would not just contradict Trump’s rhetoric; it would revive the very war logic he built his brand opposing.

The Iraq Precedent: How Wars Fail After They Begin

The Iraq War did not collapse on the battlefield. Militarily, it succeeded quickly. Baghdad fell, the regime collapsed, and the initial operation appeared decisive. The failure came later. What followed was a prolonged occupation, rising costs, political exhaustion, and a loss of strategic control.

The United States discovered that winning the opening phase of a war does not mean winning the war itself. Escalation became open-ended, exit strategies disappeared, and costs—financial and political—kept compounding. That unresolved lesson now hangs directly over Iran.

Why Iran Is a Far Bigger and More Dangerous Equation

Iran is not Iraq in 2003—not militarily, not politically, and not economically. Iran is deeply embedded in the region through state and non-state actors, proxy networks, and asymmetric capabilities. Any military strike would not remain limited or clean. Retaliation would likely be indirect, distributed, and sustained over time. More importantly, Iran’s leverage does not rest only on missiles or militias. It rests on energy geography.

Energy Is the Weapon That Moves Faster Than Missiles

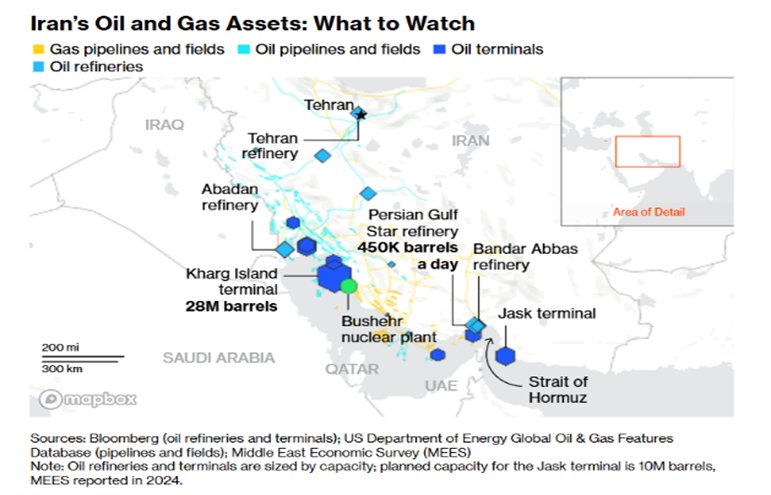

Iran sits at the heart of global energy flows. The Strait of Hormuz alone carries roughly 20% of the world’s oil supply. Disruption does not require closure; even the perception of risk is enough to move markets. This is why Iran’s conflict is treated as an oil shock first and a military conflict second.

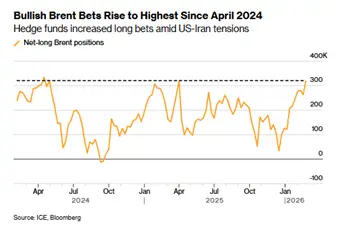

According to JPMorgan, a severe escalation scenario could push oil prices toward $120–$130 per barrel, while more extreme assumptions—including direct infrastructure damage—place upside risks even higher. Bloomberg scenarios similarly warn that sustained disruptions in Gulf flows could drive oil prices well above $100 per barrel, with secondary inflation effects spreading globally.

For the United States, this matters immediately. Higher oil prices translate directly into higher gasoline prices. Gasoline is not an abstract macro variable—it is a political pressure point. Voters see it, feel it, and react to it. A war with Iran would therefore be judged domestically not by military briefings, but by what happens at U.S. gas stations.

The Gulf’s Vulnerability: Energy Infrastructure as a Strategic Target

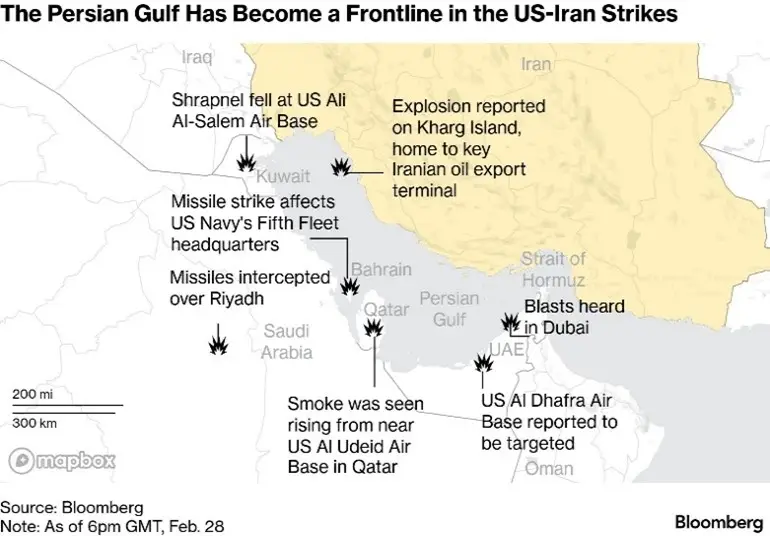

This is where the Gulf enters the equation in a far more dangerous way. Iran does not need to confront the United States head-on to escalate the conflict. It can strike what analysts often describe as the Gulf’s energy infrastructure “soft underbelly”—oil facilities, pipelines, ports, and processing hubs across the region.

Any attack on Gulf infrastructure would not only disrupt supply, but would also shatter the perception of security that underpins the region’s economic model. Investment, insurance, shipping, and long-term contracts all rely on that perception. The Gulf, therefore, is not a bystander. It is a central transmission channel

Sovereign Wealth Funds: The Silent Force Behind Capital Markets Flows

Beyond oil, the Gulf’s power today extends deep into global capital markets. Gulf sovereign wealth funds are among the largest pools of capital in the world. The GCC hosts some of the world's largest sovereign wealth funds (SWFs), with collective assets approaching $5 trillion as of early 2025, heavily driven by Abu Dhabi (ADIA, Mubadala, ADQ), Saudi Arabia (PIF), and Kuwait (KIA). The top funds are ADIA (USD 1.1 tn+), Saudi PIF (USD 900 bn - USD 1.15 tn), and KIA (USD 1tn+), which dominate global investment, particularly in technology, sports, and infrastructure.

They shape equity markets, private credit, infrastructure finance, technology investment, and global liquidity cycles. Their allocation decisions influence asset prices far beyond the Middle East. A regional war would force these funds into defensive mode—slowing deployments, repricing risk, and reallocating capital. This would tighten global financial conditions at a time when markets are already fragile.

In other words, escalation with Iran would not only shock oil markets. It would reverberate through global capital flows, amplifying volatility across equities, bonds, and emerging markets.

Israel, Iran, and Washington’s Strategic Trap

At the core of this crisis sits Israel’s strategic calculus. Iran represents Israel’s primary long-term security threat in the Middle East. From Israel’s perspective, delaying confrontation only strengthens Tehran. This creates a powerful incentive for Israel to push Washington toward action. Yet what serves Israel’s security priorities does not necessarily align with America’s economic or political constraints.

For the U.S.—and especially for Trump—the risk is being pulled into a conflict that satisfies a regional ally’s objectives while undermining domestic economic stability. For Trump, this intersects with a personal political ambition.

He does not want to be remembered as another president who failed to “solve” Iran—especially when Barack Obama pursued diplomacy through the nuclear deal, and Joe Biden sought containment and de-escalation. Trump wants to be the Republican president who had the guts to confront Iran directly—to claim victory where others hesitated. But this ambition carries extreme risk.

The Midterm Reality Trump Cannot Ignore

A prolonged Iran conflict would collide head-on with U.S. domestic politics. Rising gasoline prices, inflationary pressure, market volatility, and fiscal strain would weaken Republican prospects—especially ahead of midterm elections. Trump’s base is deeply skeptical of long wars and highly sensitive to economic pain. The same voters who cheered “America First” would not tolerate an open-ended conflict that raises household costs. This is the paradox of the Iran file. Trump may want the historic win. But he may not survive the economic fallout. The United States can strike Iran. But sustaining the consequences—economically, politically, and financially—is far harder.

The Lesson History Keeps Repeating

Iraq taught Washington that wars rarely fail at the start. They fail when leaders underestimate escalation, ignore economic transmission channels, and misjudge domestic tolerance. Iran represents a far more complex version of that same mistake. This would not be a short war. It would not be a contained war. And it would not be cheap.

History is not repeating itself exactly. But it is close enough to demand caution—because this time, the costs will be higher, broader, and faster.