This Is Not De-escalation… It’s Repricing of Risk

What markets are interpreting as de-escalation is, in reality, a transition from dynamic risk to structural risk. The fragile US–Iran ceasefire, unresolved tensions in Lebanon, and repeated disruptions around Hormuz — including vessel seizures and near-standstill shipping — suggest that the region has not stabilized. It has simply moved into a phase where risk is less visible, but more embedded. This distinction matters. Because markets can price events… but struggle to price persistent uncertainty.

Oil Is Now the Transmission Channel of Geopolitics

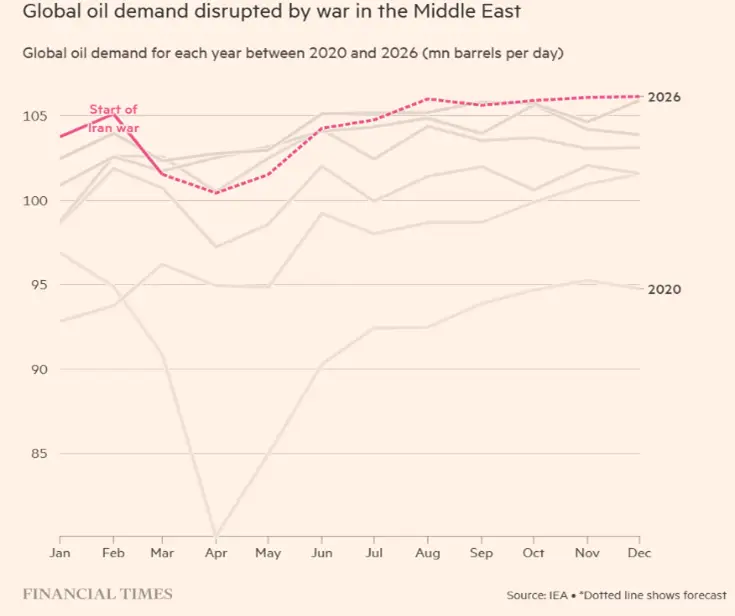

The key shift is not higher oil prices — it is how oil now transmits geopolitical shocks into the global macro system.

Both the International Monetary Fund and the World Bank are no longer anchoring forecasts around a single baseline. Instead, they are explicitly modeling scenario dispersion, reflecting how sensitive the system has become to supply disruptions.

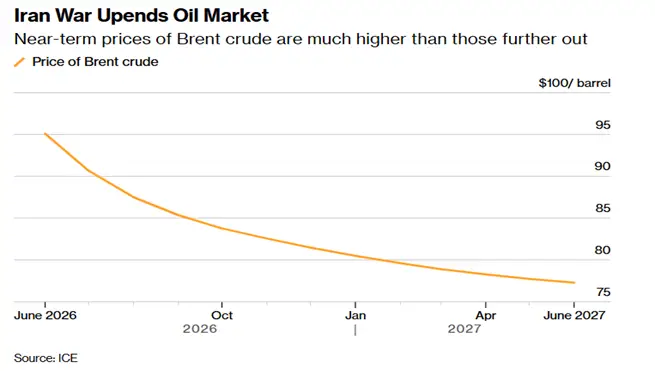

At $90 oil, the shock is contained. At $100–110, inflation persistence forces central banks to delay easing. Beyond that, the global economy enters a policy trap: tightening into weakness or tolerating inflation. The implication: Oil is no longer cyclical — it is structural to policy decisions

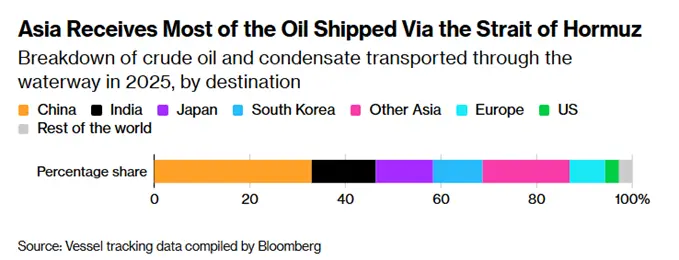

Hormuz Is Fragmenting the Region Economically

The Strait of Hormuz is no longer a shared bottleneck — it is a differentiator of economic resilience. The region is effectively splitting into four macro profiles:

- Iran and Oman are benefiting from price dynamics despite constraints, capturing upside from disruption.

- Saudi Arabia and the UAE are leveraging partial rerouting infrastructure, transforming price volatility into a stabilizing mechanism.

- Qatar and Kuwait remain exposed operationally but insulated financially through sovereign buffers.

- Iraq and Bahrain face a direct transmission of disruption into fiscal and external balances, with limited shock absorption capacity.

The same shock is producing asymmetric macro-outcomes which will reshape capital allocation across the region.

From Global Capital to Geopolitical Capital

A more profound shift is happening beneath the surface: capital is being re-politicized. Recent financial flows across the region — from bilateral support packages to strategic investments — indicate that liquidity is increasingly secured through alliances rather than markets. In periods of high uncertainty, private capital becomes risk averse. Sovereign capital steps in — but not neutrally. This marks a transition from: efficient capital allocation → strategic capital deployment. With long-term implications for:

- Credit risk pricing

- Sovereign spreads

- And investment flows across emerging markets

Trade Is Moving from Efficiency to Security

Global trade architecture is undergoing a forced reset. Hormuz disruptions have exposed the fragility of hyper-efficient supply chains that depend on a limited number of chokepoints. As a result, countries are accelerating investments in alternative corridors — pipelines, ports, and regional trade routes — even at a higher cost. This is not a temporary adjustment. It is a structural shift toward redundancy and control.

The consequence:

- Higher global trade costs

- Lower efficiency

- Increased regionalization of trade

In other words, globalization is not reversing —it is fragmenting.

The Gulf’s Strategic Learning Curve

The Gulf is not just reacting to the conflict — it is recalibrating its entire economic model.

- First, security assumptions are being rewritten. The reliability of external protection is no longer taken for granted, accelerating investment in autonomous defense capabilities and diversified alliances.

- Second, energy dominance is being reinterpreted. Oil remains a source of power — but also a source of vulnerability when tied to chokepoints.

- Third, sovereign wealth is evolving from a return-seeking portfolio into a multi-objective instrument — balancing financial returns with geopolitical influence and domestic stability.

This marks a shift from a model built on abundance to one built on resilience and control.

What the Gulf Will Do Next: Structural Shifts, Not Cyclical Moves

The next phase is unlikely to be reactive — it will be strategic. Infrastructure investments will increasingly focus on bypassing chokepoints and securing export routes. Defense spending will expand, not just on scale but in technological sophistication, integrating AI and early-warning systems. At the same time, capital allocation will tilt toward domestic and regional priorities, particularly in sectors that enhance economic sovereignty — logistics, energy security, and strategic technologies. The objective is clear: reduce exposure to external shocks without sacrificing global influence.

MENA is Being Reclassified in Real Time

The broader Middle East is undergoing a silent reclassification Countries are no longer assessed purely on growth prospects — but on their ability to navigate geopolitical risk, secure liquidity, and maintain external balances under stress. This is creating a three-tier structure:

- Core economies with capital and resilience

- Vulnerable economies reliant on external support

- Transitional economies balancing both dynamics

The region is not converging; it is diverging structurally.

The Global Implication: A More Fragile Equilibrium

What is unfolding in the Gulf does not stay in the Gulf. Higher oil volatility feeds directly into global inflation. Delayed monetary easing tightens financial conditions. And fragmented trade flows reduce global efficiency. The result is a more fragile global equilibrium —where shocks travel faster, last longer, and are harder to absorb.

The Bottom Line: Stability Is No Longer the Base Case

Markets are still pricing stability as the central scenario. But structurally, stability has become conditional not given. The region has entered a phase where: risk is persistent alliances shape outcomes and economic strategy is inseparable from geopolitics. The missiles may have slowed…but the system has already changed.