A strong non-farm payroll (NFP) didn’t support a higher USD

Stronger payrolls were expected, but cracks emerged as unemployment rose to 3.7% and average hourly earnings weakened.

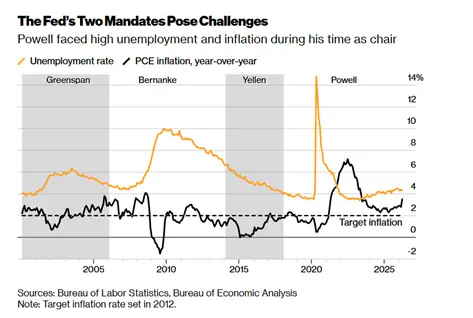

It would seem the Fed has some breathing room before the next CPI release. However, a more expedient approach from the ECB is necessary with the need to hike rates by 75bp in order to maintain credibility. Eurozone inflation hit 9.1%, but there could be some downside risks as European gas prices eased on fiscal initiatives. Indeed, the credibility catch-up remains a theme after Powell’s hawkish comments at Jackson Hole.

The slump in JPY to a 24-year low comes just as GBP is targeting lows not seen since 1985. The bearish UK view is premised on recession risks, soaring inflation, dependence on foreign capital and a BoE mandate that is set to be circumscribed. The political paralysis ought to be partly unlocked as the UK will soon announce its new Prime Minister on Monday, which will see Boris Johnson officially resign on Tuesday at the Queen’s estate in Balmoral.

In spite of a stronger USD over the week, we saw EM across FX, rates and credit outperform developed markets, but equities remained weak (S&P -5.5%) and crude oil languished (-6.3%). In fact, oil is on its longest monthly losing streak since 2020 (-9% in August), as growth concerns rise, an Iranian nuclear agreement becomes increasingly realistic and the G7 introduced a cap on Russian oil prices. PMI trends were generally upbeat as China’s Caixin Manufacturing reading was steady, just as South Africa’s vastly recovered. This helped offset the surprising slump in South Korean and Taiwanese PMIs. We would also note that Indonesia’s upbeat PMI of 51.7, came with headline inflation retreating from 4.94% to 4.69%. South Africa’s PMI of 52.1 was driven by higher business activity which rose from 39.8 to 50.6, just as business conditions improved from 49.4 to 57.9 and purchasing commitments rose from 45.4 to 54.9.

Sweden announces emergency support for energy producers

EU also considering action as rising collateral demands prompt policymakers to warn of ‘financial stability threat’.

Sweden will give emergency liquidity support to electricity producers as its prime minister warned that Russia’s decision to halt gas deliveries to Europe could place its financial system under severe strain. The government would offer hundreds of billions of kroner in funding to electricity producers, who have seen the amount of collateral they must post with exchanges balloon in response to soaring gas and power prices and increasing volatility.

EU energy ministers will also consider taking steps to ease the lack of liquidity for energy companies across the bloc at an emergency meeting on Friday, according to two officials briefed on the discussions. Noting that rising collateral demands for electricity producers could ripple through the main Nasdaq Clearing market in Stockholm and, in the worst case, spark a financial crisis. This came into action after Russia said on Friday that it would no longer supply gas via the Nordstream 1 pipeline. That announcement came after energy markets had closed for the weekend.

Russia indefinitely suspends Nord Stream gas pipeline to Europe

Russia has indefinitely suspended natural gas flows through the Nord Stream 1 pipeline, exacerbating a squeeze on Europe’s energy supplies and deepening the recession risks faced in the EU.

State-owned Gazprom, which was meant to restore operations on the Baltic Sea pipeline on Saturday after three days of maintenance, said the suspension was due to a technical fault. The move came hours after the G7 countries said they were pushing ahead with a plan to try to impose a price cap on Russia’s oil exports as part of an attempt to lower revenues flowing to Moscow that can be used to fund its invasion of Ukraine.

It will heighten fears in European capitals that Russia aims to further cut supplies before the winter. Moscow has been accused of “weaponising” its gas to stoke a cost-of-living crisis in retaliation for western support for Ukraine. Russia’s president Vladimir Putin has made little attempt to hide his goal to undermine western sanctions and stop attempts by Ukraine’s allies to reduce their dependence on Moscow’s oil and gas exports.

Gazprom had already cut capacity on Nord Stream 1 since June, curtailing volumes to just 20 per cent of normal levels and triggering a more than doubling in European gas prices. The company said the shutdown was because of an oil leak discovered in the main gas turbine at the Portovaya compressor station near St Petersburg, which feeds the line that runs through the Baltic Sea to Germany. However, Siemens Energy, which manufactures and maintains the turbines that power the pipeline, cast doubt on this explanation. After jumping last week to an all-time high, European gas prices have slid in recent days, declining by a third to 209 EUR per megawatt hour — though that is still about 10 times the average level of the past decade. Prices eased partly as the EU hit its target of filling storage sites to 80 per cent of capacity ahead of the winter heating season. But gas stocks in storage alone are not enough to meet winter demand without normal Russian export flows.

Sri Lanka and Zambia make progress in securing IMF financial support

On Thursday, IMF staff and the Sri Lankan authorities reached a staff-level agreement (SLA) to support Sri Lanka’s economic adjustment with a 48-month Extended Fund Facility (EFF) of about $2.9 billion. A day earlier, IMF’s Executive Board approved a 38-month Extended Credit Facility (ECF) for Zambia of around $1.3 billion, equivalent to 100% of Zambia’s IMF quota. Zambia had achieved a SLA with the IMF in December 2021.

These developments represent credit-positive steps for distressed sovereigns. In 2020, Zambia became one of the first pandemic-era emerging markets sovereign defaulters when the government asked for a debt moratorium and initiated a restructuring process under the guidelines of the G20’s so called “Common Framework” that brings together official sector creditors from the Paris Club (developed markets creditor nations) and China. In that context, successful implementation of the new ECF arrangement is subject to Zambia securing timely restructuring agreements with external creditors.

Sri Lanka, whose government formally defaulted and requested IMF assistance in July 2022, is facing a similar set of challenges in terms of negotiating with bi-lateral and private creditors. While reaching the SLA was a critically important step on the way to securing IMF funding and restoring debt sustainability, the Sri Lankan authorities still need to achieve significant progress before IMF disbursements materialize. The Fund has made it clear that financing assurances to restore debt sustainability from Sri Lanka’s official creditors (China, India and Japan being the largest ones) and making a good faith effort to reach a collaborative agreement with private creditors are crucial before the IMF can deem Sri Lanka’s sovereign debt sustainable and provide financial support.

Chile secures $18.5 billion IMF Flexible Credit Line (FCL) as it heads into referendum on new constitution

On Monday, the IMF approved a two-year FCL for Chile worth 18.5 billion USD. This coming Sunday, September 4, a referendum will decide whether a new constitution for the country, being drafted by an elected Constitutional Convention since May 2021, will be approved, or rejected.

According to the latest polls, it appears the more likely outcome of Sunday’s plebiscite will be to reject the proposed new constitution intended to replace the existing Pinochet-era charter. In the case of a rejection, we expect a mixed impact from a market perspective. On one hand, the proposed new constitution implies a structural increase in government spending and participation in economic affairs, so markets are likely to react positively to its potential rejection by voters.

On the other, a rejection would mean a major political defeat for President Boric who has thrown his political support behind the new constitution. As such, if Chileans vote to reject the constitutional proposal, this would be another heavy political blow to the Boric Administration, which has already seen a significant decline in their approval ratings and will likely face even stronger governance and policy-implementation challenges in that scenario.

Against this complicated domestic political backdrop and significant global macro cross currents, the 18.5 billion USD FCL from the IMF provides a welcome support to Chile’s external accounts. It comes at a time when the economy is struggling with record high Current Account (CA) deficits, weakness in Chile’s main commodities export market with China, and pressure on FX reserves amid the Central Bank’s 25 billion USD FX intervention program initiated in July. In this context, we expect the FCL to reduce pressure on Chile’s FX/sovereign credit but not drive a sustained rally in the near-term, given a variety of meaningful headwinds.

Stay up to date

More Newsletter to Check

SUBSCRIBE TO NEWSLETTER

Subscribe to download our daily economics and business roundup

×

![]()