Global Markets Balance Optimism with Underlying Risks

Global markets showed cautious optimism this week, driven by progress on U.S.–China trade talks and the announcement of a new U.S.–UK trade deal. Hopes for fiscal support in Congress added to the positive tone. Stocks rose, Treasury yields climbed to around 4.35%, and the dollar strengthened to near 101 on the DXY. Oil stayed above USD 60, while gold flattened as demand for safe havens eased. The Federal Reserve held rates steady, and Jerome Powell stressed a patient, data-dependent approach, even as inflation and job market risks linger. Economic data was mixed: services activity improved, but the trade deficit widened to its largest in over a decade. Consumer borrowing rose, signaling both strong spending and financial strain. Jobless claims held steady, but layoffs in key sectors raised concerns. In Europe, Germany’s political landscape appeared fragile after a rare second-round vote for the new Chancellor. However, economic data surprised on the upside with stronger factory orders and industrial output. The Bank of England cut rates by 25 bps but showed internal divisions. In Asia, tensions resurfaced between India and Pakistan, while the Taiwanese dollar strengthened. China’s services sector slowed, prompting targeted monetary easing. Despite U.S. tariffs, China’s exports rose 8.1% YoY by shifting trade toward Southeast Asia. Imports dropped slightly, keeping the trade surplus high.

EM High Yield Leads Gains While Romania Underperforms

Emerging market (EM) hard currency sovereign debt posted a modest gain of +0.3% this week, mainly driven by a strong rebound in the high yield segment (+0.7%) as investor sentiment improved. In contrast, investment grade sovereigns saw a slight decline (-0.1%). Sovereign spreads narrowed by 12 basis points overall, with high yield tightening by 21 bps versus a smaller 5 bps for investment grade. Latin America and Africa led the gains, particularly high-risk names like Venezuela, Ecuador, Ghana, and Senegal. Romania was the main underperformer due to rising political risks, concerns over fiscal reforms, and the growing support for euro-skeptic candidate George Simion. EM local currency debt slipped by -0.2%, impacted by the stabilization of the U.S. dollar. Romania also led losses in local currency markets. EM corporate debt underperformed sovereigns, delivering a smaller return of +0.1%, with high yield up +0.2% and investment grade flat. Corporate spreads tightened slightly by 6 bps. The corporate primary market remained active, with nine new issuers this week. However, no new sovereign deals were recorded.

Aramco’s Profit Slides as Oil Weakens, Straining Saudi Finances

Saudi Aramco reported a 4.6% drop in Q1 net income to SAR 97.5 bn (USD 26 bn), mainly due to lower crude prices. While operating profit beat expectations, free cash flow couldn’t fully cover dividends, which were already reduced. The quarterly dividend fell to USD 21.36 bn, down from USD 31 bn a year ago, as the company scaled back performance-linked payouts. This adds pressure on Saudi Arabia’s budget, which relies heavily on Aramco’s dividends to fund its ambitious spending plans, including the Neom project and investments in sports. Despite recent oil production hikes, Brent crude prices have dropped significantly — hovering near USD 64, well below the IMF’s USD 92 breakeven estimate for Saudi Arabia. Aramco sold crude at an average of USD 76.30 in Q1, compared to USD 83 a year earlier. With debt levels rising and a widening fiscal deficit, the Kingdom faces mounting financial strain. This comes ahead of President Trump’s visit to Riyadh, where he’s expected to push OPEC+ to increase output to lower prices and contain inflation.

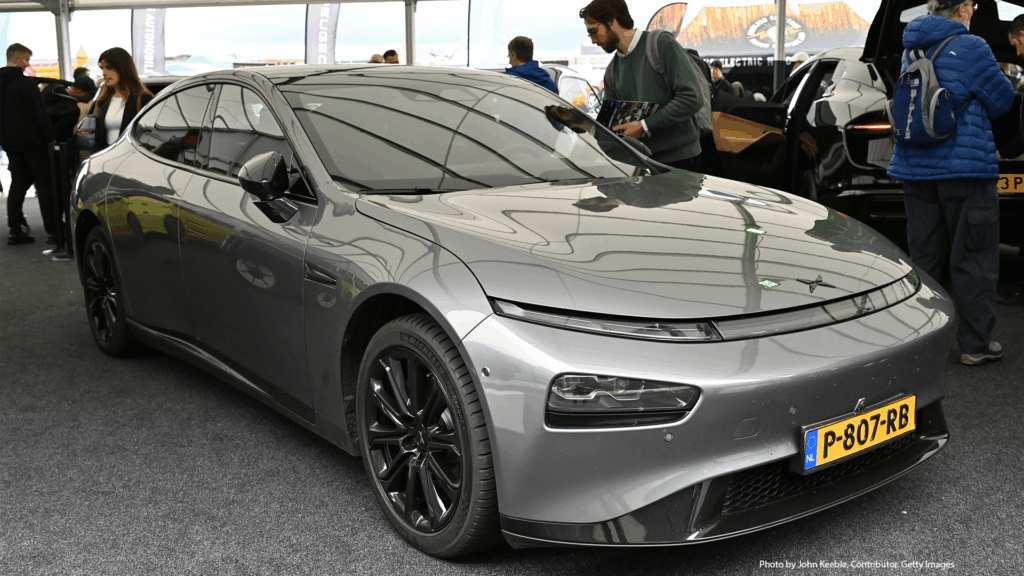

Chinese Carmakers Shift Gears in Europe – From EVs to Combustion Engines

Chinese automakers are ramping up sales of hybrid and combustion engine cars in Europe, even as demand for their electric vehicles (EVs) slows. In Q1 2025, Chinese brands registered over 150,000 vehicles in Europe – a new record – but only 30% of those were EVs, the lowest share since early 2020. This shift comes after the EU imposed steep tariffs on Chinese-made EVs, citing unfair subsidies from Beijing. Automakers like BYD and SAIC’s MG brand are now focusing more on plug-in hybrids and combustion models, with MG more than doubling its sales of these types in the EU, while its EV sales halved. Rising tariffs (up to 45% in some cases) are one reason for the change, but the trend also reflects broader European consumer preferences shifting toward hybrids. The new strategy has helped Chinese brands grow their market share, surpassing 5% of European car sales for the first time. Despite the slowdown in EV momentum, BYD and others are still seeing growth in electric model registrations. To offset tariffs, BYD is expanding its production in Europe with new factories in Hungary and Turkey, and is considering more. Chinese carmakers are adapting quickly to a changing regulatory and market landscape, challenging European giants like Volkswagen and Stellantis across multiple segments.

Markets Brace for a Pivotal Week of Geopolitics and Data

Global markets are heading into a high-stakes week shaped by geopolitics and key economic updates. All eyes will be on U.S.–China trade talks in Switzerland for signs of de-escalation, while President Trump’s Middle East visit could sway energy markets and geopolitical risk. In the U.S., inflation, retail sales, industrial production, and consumer sentiment data will give insight into how tariffs are affecting the real economy. Walmart and other corporate earnings will also reflect consumer trends. Meanwhile, comments from Fed Chair Powell and governors may help clarify the Fed’s policy stance. In Europe, finance ministers meet in Brussels as markets analyze GDP, industrial output, and the ZEW sentiment survey. The UK will publish its Q1 GDP and industrial production. Asia sees major releases from Japan (Q1 growth and output) and China (April CPI and PPI), expected to confirm deflation pressures despite a possible credit rebound. In the Philippines, midterm elections could solidify President Marcos Jr.’s legislative power. In emerging markets, Mexico’s central bank (Banxico) is expected to cut rates by 50 bps, while Türkiye’s current account data will provide insights into its external balances.

تفاؤل حذر في الأسواق العالمية رغم المخاطر الكامنة

شهدت الأسواق العالمية هذا الأسبوع تفاؤلًا حذرًا، بدعم من تقدم المفاوضات التجارية بين أمريكا والصين، واتفاق جديد بين أمريكا وبريطانيا. التوقعات بإجراءات مالية جديدة في الكونغرس دعّمت المزاج الإيجابي. ارتفعت الأسهم، وصعد عائد السندات إلى 4.35%، بينما قفز الدولار إلى قرب مستوى 101. واستقرت أسعار النفط فوق 60 دولارًا، بينما هدأ الطلب على الذهب. الفيدرالي الأميركي ثبت أسعار الفائدة، وباول أكد على نهج حذر يعتمد على البيانات، رغم استمرار مخاوف التضخم وسوق العمل. البيانات الاقتصادية جاءت مختلطة: نشاط الخدمات تحسّن، لكن العجز التجاري اتسع لأعلى مستوى منذ أكثر من عقد. وارتفع الاقتراض الاستهلاكي، ما يعكس استمرار الإنفاق رغم الضغوط المالية. طلبات البطالة استقرت، لكن ظهرت إشارات تسريح في قطاعات مهمة. في أوروبا، أظهرت السياسة هشاشة بعد جولة تصويت ثانية لاختيار المستشار الألماني، لكن البيانات الاقتصادية في ألمانيا جاءت أفضل من المتوقع. بنك إنجلترا خفّض الفائدة 25 نقطة أساس، مع انقسام داخلي بين أعضائه. في آسيا، تصاعدت التوترات بين الهند وباكستان، وارتفعت العملة التايوانية. وأظهرت بيانات الصين تباطؤًا في قطاع الخدمات، ما دفع البنك المركزي لتخفيف السياسة النقدية. ورغم الرسوم الأميركية، ارتفعت صادرات الصين بنسبة 8.1% بفضل توجيهها نحو جنوب شرق آسيا، بينما تراجعت الواردات بشكل طفيف، ما أبقى الفائض التجاري مرتفعًا

أدوات الدين مرتفعة العائد تقود المكاسب ورومانيا تتراجع

سجلت أدوات الدين السيادية بالعملات الصعبة في الأسواق الناشئة ارتفاعًا طفيفًا هذا الأسبوع بنسبة +0.3%، بدعم من أداء قوي لفئة السندات مرتفعة العائد (+0.7%) مع تحسن شهية المخاطرة. في المقابل، تراجعت السندات المصنفة استثماريًا بشكل طفيف (-0.1%). وقلصت الفروق السيادية 12 نقطة أساس، بقيادة تقلص بـ21 نقطة في مرتفعة العائد، مقابل 5 نقاط فقط للمصنفة استثمارية. لاتين أمريكا وأفريقيا قادتا المكاسب مجددًا، خاصة سندات الدول عالية المخاطر مثل فنزويلا، الإكوادور، غانا، والسنغال. بينما كانت رومانيا الأضعف أداءً بسبب عدم الاستقرار السياسي ومخاوف بشأن الإصلاحات المالية، وتزايد دعم المرشح الشعبوي المعادي لأوروبا جورج سيميون. أما أدوات الدين المحلية، فسجلت تراجعًا طفيفًا بنسبة -0.2% مع استقرار قوة الدولار، وكانت رومانيا أيضًا الأضعف أداءً. سندات الشركات الناشئة جاءت خلف السيادية، بعائد إجمالي +0.1%، حيث ارتفعت مرتفعة العائد +0.2% وظلت المصنفة استثمارية دون تغيير. تقلصت الفروق بنحو 6 نقاط أساس دون اختلاف كبير بين الفئتين. واستمر النشاط في السوق الأولية للشركات، مع إصدار 9 شركات جديدة هذا الأسبوع، بينما لم تُسجل أي إصدارات سيادية.

تراجع أرباح أرامكو يزيد الضغوط على ميزانية السعودية

سجلت أرامكو السعودية انخفاضًا بنسبة 4.6% في أرباح الربع الأول لتصل إلى 97.5 مليار ريال (26 مليار دولار)، نتيجة تراجع أسعار النفط. ورغم أن الأرباح التشغيلية فاقت التوقعات، إلا أن التدفقات النقدية لم تغطِ بالكامل توزيعات الأرباح. انخفضت توزيعات الأرباح إلى 21.36 مليار دولار مقارنة بـ31 مليار دولار في نفس الفترة من العام الماضي، بعد تقليص الحوافز المرتبطة بالأداء. هذا الانخفاض يزيد من الضغط على ميزانية المملكة، التي تعتمد بشكل كبير على أرباح أرامكو لتمويل مشاريعها الطموحة مثل “نيوم” والاستثمار في قطاع الرياضة. ورغم زيادة إنتاج النفط مؤخرًا، تراجعت أسعار برنت إلى نحو 64 دولارًا، وهي أقل بكثير من مستوى 92 دولارًا الذي تحتاجه السعودية لتحقيق التوازن المالي بحسب صندوق النقد الدولي. وباعت أرامكو النفط في الربع الأول بسعر متوسط 76.30 دولار للبرميل، مقابل 83 دولارًا العام الماضي. تزامنًا مع هذه التحديات، تتصاعد الضغوط المالية على المملكة في ظل ارتفاع مستويات الدين واتساع العجز. ومن المتوقع أن يضغط الرئيس الأميركي ترمب، خلال زيارته للرياض هذا الأسبوع، على “أوبك+” لزيادة الإنتاج وخفض الأسعار بهدف كبح التضخم والضغط على روسيا.

شركات السيارات الصينية تغيّر استراتيجيتها في أوروبا من الكهرباء إلى البنزين

بدأت شركات السيارات الصينية تركز بشكل أكبر على بيع السيارات الهجينة والتي تعمل بمحركات احتراق داخلي في أوروبا، في ظل تباطؤ الطلب على السيارات الكهربائية. خلال الربع الأول من عام 2025، تم تسجيل أكثر من 150 ألف سيارة صينية في أوروبا – وهو رقم قياسي – لكن السيارات الكهربائية شكلت فقط 30% من هذا الرقم، وهو أدنى مستوى منذ عام 2020. هذا التحول جاء بعد فرض الاتحاد الأوروبي رسوم جمركية عالية على السيارات الكهربائية الصينية، بدعوى أنها تستفيد من دعم حكومي غير عادل. شركات مثل BYD وMG (التابعة لـSAIC) أصبحت الآن تركز على السيارات الهجينة والعادية، حيث ضاعفت MG مبيعاتها من هذه الفئات بينما انخفضت مبيعاتها من السيارات الكهربائية للنصف. وبجانب الرسوم المرتفعة (التي تصل إلى 45%)، يلاحظ أيضًا أن الطلب على السيارات الهجينة في أوروبا أصبح أكبر، ما دفع الشركات الصينية لتكييف استراتيجيتها. ونتيجة لذلك، تخطت حصة الشركات الصينية 5% من سوق السيارات الأوروبية لأول مرة. رغم التباطؤ في نمو سوق السيارات الكهربائية، لا تزال BYD وغيرها تسجل زيادات في مبيعاتها من هذه الفئة. وتعمل BYD على بناء مصانع جديدة في المجر وتركيا لتفادي الرسوم، وتفكر في إنشاء مصنع ثالث في أوروبا. شركات السيارات الصينية تواصل التوسع السريع في أوروبا، متحدّية عمالقة الصناعة مثل فولكس فاجن وستيلانتس، ومتنقلة بذكاء بين السيارات الكهربائية والهجينة والبنزين حسب تغير السوق.

الأسواق تستعد لأسبوع حاسم مليء بالبيانات والتوترات الجيوسياسية

تدخل الأسواق أسبوعًا مهمًا مع تزايد الترقب لمجموعة من التطورات الجيوسياسية والاقتصادية. الأنظار تتجه إلى محادثات التجارة بين أميركا والصين في سويسرا بحثًا عن أي مؤشرات على التهدئة، بينما قد تؤثر جولة ترمب في الشرق الأوسط على أسواق الطاقة والمخاطر الجيوسياسية. في الولايات المتحدة، بيانات التضخم، مبيعات التجزئة، الإنتاج الصناعي، وثقة المستهلك ستكشف كيف تؤثر التعريفات الجمركية على الاقتصاد الفعلي. نتائج الشركات مثل Walmart ستعطي إشارات مهمة عن وضع المستهلك، في حين أن تصريحات باول وأعضاء الفيدرالي قد تساعد في فهم توجهات السياسة النقدية. في أوروبا، يجتمع وزراء المالية في بروكسل مع صدور بيانات الناتج المحلي والإنتاج الصناعي، بالإضافة إلى نتائج مؤشر ZEW لثقة المستثمرين. كما تُصدر المملكة المتحدة بيانات النمو والإنتاج للربع الأول. أما في آسيا، فتعلن اليابان أرقام النمو والإنتاج، فيما يُتوقع أن تؤكد بيانات الصين (CPI وPPI لشهر أبريل) استمرار الضغوط الانكماشية رغم تحسن متوقع في الإقراض. وفي الفلبين، الانتخابات النصفية قد تعزز من سيطرة الرئيس ماركوس على البرلمان. في الأسواق الناشئة، يتوقع أن يخفض البنك المركزي المكسيكي (Banxico) الفائدة 50 نقطة أساس، بينما تصدر تركيا بيانات الحساب الجاري لتوضيح وضعها الخارجي.

Stay up to date

More Newsletter to Check

SUBSCRIBE TO NEWSLETTER

Subscribe to download our daily economics and business roundup

×

![]()